Orlando, Fla. — Of course well all know that Santa knows when you’ve been bad or good. He also knows that whether or not you have been good all year, a business insurance policy is the best way to cover the structure or your workshop if it’s damaged by any insured disaster. A business policy would also provide protection for liability in unexpected events, like if customers or a delivery person, as an example, is injured in a fall and sues ‘Santa.’

As the CEO of his workshop, Santa himself should have key person insurance, and so should you. This provides insurance protection in case a key person “whose services are essential to the continuing success of a business” dies or becomes ill. And, as much as Santa is the most important person during the holidays in the North Pole and abroad, we are sure in your business, your are just as essential to your operation as well as any other designated personnel.

Especially if your business is a retail operation which happens to sell toys or items that can be considered gifts for children, there are other types of liability coverage could prove useful too: product liability.

As an example,

Santa discovered that this type of insurance coverage protects his business if one of the toys made in his workshop is defective and injures some good little girl or boy; product recall insurance can help cover the cost of taking back defective gifts; and professional liability can help Santa safeguard his business if a parent tries to sue Santa because he delivered the wrong toy.

According to a February 2015 report from the advocacy group Kids in Danger, recalls of children’s products declined 34 percent in 2014 to 75, the lowest number in the 14 years of data collected by the organization, which is extraordinarily good.

In 2014 there were 338 incidents reported prior to recall of the 75 children’s products, for an average of 5 incidents per recalled product. The 2014 average represents an improvement from 2013, when the average was 14 incidents per recalled product. Injuries related to the recalls were down 85 percent, and deaths fell from 11 in 2013 to three in 2014. Children’s product recalls in 2014 totaled almost 17 million units.

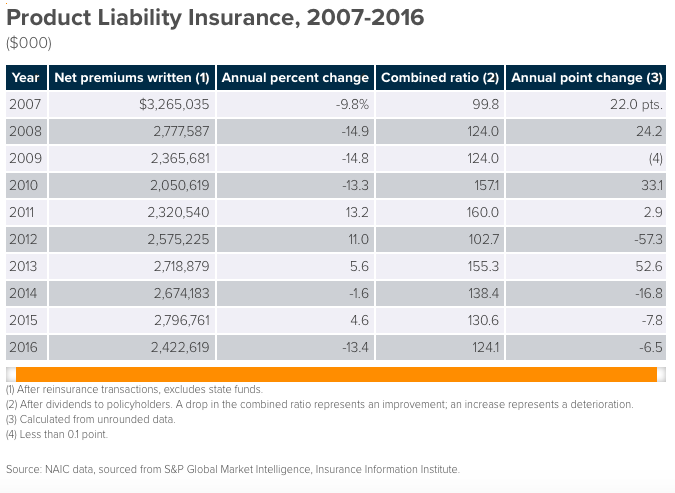

The following chart gives you an idea of how the insurance industry had reflected and adjusted to risk variation.

The Travelers Insurance 2015 Business Risk Index showed that legal liability was the fourth-highest rated worry for business leaders in the United States, down from No. 3 a year earlier.

In the 2016 risk survey, businesses reported being less guarded in their risk outlook than previous years. However, two emerging trends – a changing workforce and the fast pace of technological change – are viewed as posing the greatest risks to businesses over the next five years.

Top worries were consistent with 2015 results, with small business owners typically worrying less about the top risks. All businesses still worry most about medical cost inflation and the rising cost of employee benefits. They also worry about cyber risks, including data breaches; legal liability; and the challenge of attracting talented and skilled staff – although the levels of worry on those risks have declined by several points.

Nevertheless, you are better off having a plan to respond to these kind of unfortunate events, having your insurance coverage in good standing, in case this trend changes, as you can see it has happened in the past.

Remember that your insurance premium is affected by the level of risk, which means you might find less expensive options now than what you’ve seen in the past.

For personal insurance solutions check out our sister company Orlando Insurance Center